/Passle/5a1c2144b00e80131c20b495/MediaLibrary/Images/2025-09-04-12-58-34-038-68b98cfabb695430b1bc5a13.png)

Pillar Two proposals: what you need to know

5 minute read

Pillar Two of the OECD/G20 agreement on international tax reform aims to put a floor on tax competition and end a “race to the bottom”.

The main component of Pillar Two is the GloBE rules. They aim to ensure that large MNE groups pay a minimum effective tax rate (ETR) of at least 15% on their profits in every jurisdiction in which they operate.

This will be achieved by allowing countries to impose top-up taxes in situations where an MNE is taxed below the minimum rate.

Pillar Two also includes the subject to tax rule (STTR). This will apply before the GloBE rules and will give greater source taxing rights to certain developing countries.

Why is this happening now?

The global minimum tax under Pillar Two satisfies a long-held ambition of many countries to prevent their corporate tax bases from being eroded as a result of competition from jurisdictions that seek to attract highly profitable, mobile business activities with a combination of low tax rates and generous incentives.

It was proposed by G20 governments as a response to public concerns about MNE tax avoidance. Covid-19 has given the international discussions added impetus as governments eye a potentially valuable source of new revenues to fund recovery and fiscal consolidation.

What have governments committed to do?

137 countries have endorsed the October 2021 OECD Inclusive Framework statement which sets out the core features of the GloBE rules. The statement is a political commitment. It doesn't require countries to introduce the GloBE rules, however it does require them to accept the application of the rules by other countries, and to act consistently with the GloBE design if they implement the rules themselves.

The OECD intends to develop an implementation framework for Pillar Two during 2022, with a view to the rules coming into effect during 2023. We expect that many countries - including the UK and the EU - will aim to implement the rules on that timetable.

Who will the GloBE rules apply to?

The GloBE rules will apply to groups with entities in more than one jurisdiction and revenues of at least €750m per annum.

This will be subject to limited exclusions:

- a de minimis, which will exclude jurisdictions where the group has revenues of less than €10m and profits of less than €1m from the GloBE calculation;

- a limited exclusion for groups in the early stages of international expansion (<€50m tangible assets overseas and operating in no more than five other jurisdictions); and

exclusions for pension funds, investment entities, and governmental and intergovernmental organisations.

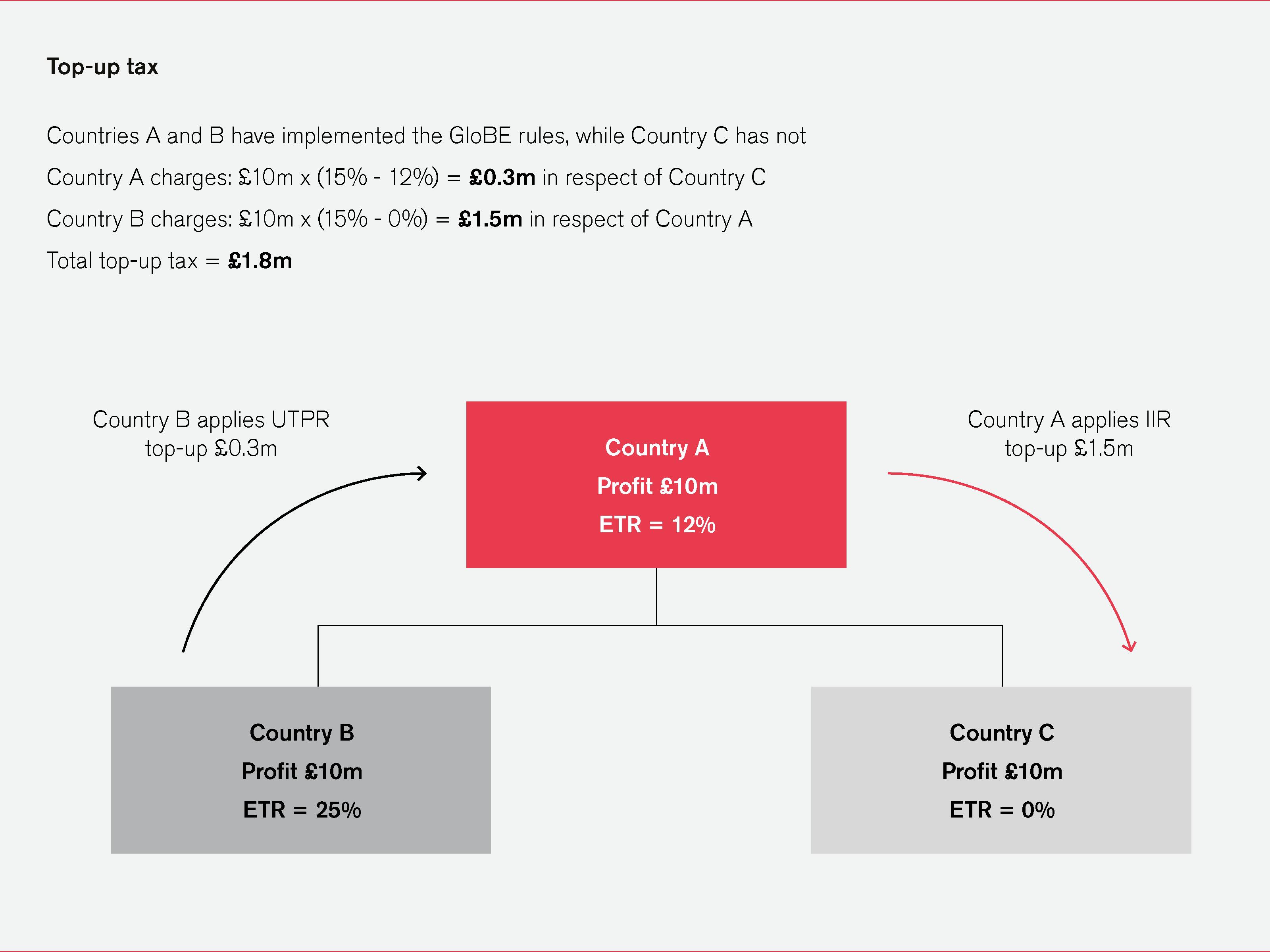

What are the GloBE rules?

The GloBE rules will determine an amount of top-up tax to be paid by a group. That will be done by:

- testing the effective tax rate (ETR) paid by the group in each jurisdiction in which it operates;

- determining how much additional tax, if any, should be paid to increase each jurisdiction's ETR to 15%; and

- allocating that top-up tax to other jurisdictions.

Top-up tax will be allocated under two rules:

The main rule is the income inclusion rule (IIR). This is analogous to the controlled foreign companies (CFC) rules that many countries already apply. It will generally be applied by the home jurisdiction of the ultimate parent entity (UPE) in a corporate group and give them the right to collect all the top-up tax relating to foreign entities owned by the UPE.

There is also a backup rule - the undertaxed payment rule (UTPR). The UTPR will allocate any top-up tax that hasn't been allocated under the IIR. That could be top-up tax due in relation to:

- profits earned in the UPE jurisdiction, in situations where the UPE jurisdiction doesn't apply an ETR of at least 15%; or

- profits earned by the entire group, in situations where the UPE jurisdiction doesn't implement the GloBE rules.

Any top-up tax due under the UTPR will be allocated among the countries in which the group has operations in proportion to the group's payroll costs and tangible asset value in each country. Those countries will then collect the tax either by denying deductions to, or imposing a schedular charge on, group entities resident in their territory.

How will ETR be measured?

ETR = Covered tax / GloBE profit

Covered tax will include both current and, in some instances, deferred taxes accrued in a company's accounts. Including deferred tax reduces the likelihood that a top-up tax is imposed solely because of differences in when income and expenses are recognised under the GloBE and domestic tax rules.

GloBE profit will be based on accounting profit before tax, subject to adjustments - most significantly a participation exemption for dividends and gains derived from shareholdings of more than 10%.

Substance-based income exclusion

A formulaic substance carve out will exclude a fixed return on a group's tangible assets and payroll costs in a jurisdiction from the profits that are subject to the top-up tax. This recognises that income attributable to such physical factors is unlikely to result from profit shifting.

What about the subject to tax rule?

At the behest of developing countries, Pillar Two also includes the subject to tax rule (STTR). This is not concerned with imposing top-up tax. Instead, it amends existing bilateral tax treaties to give source countries greater taxing rights in relation to certain related party payments. The final list of covered payments is still to be published, but it will include interest and royalties.

Importantly, the STTR may only be invoked by developing countries, and only to amend treaties with jurisdictions that tax the covered payments at a nominal rate below 9%.

Read our more detailed Q&A guide to explain the application of the model rules.

Keep up to date with the latest developments and other useful information on our BEPS 2.0 hubpage.

Authors

{kind=link}

Related topics

Like what you are reading?

Stay up to date with our latest insights, events and updates – direct to your inbox.

How can we help you?

Browse our people by name, team or area of focus to find the expert that you need.